Hello. This is Stanton Jones and Sunder Sarangan with what’s important in the IT and business services industry this week.

If someone forwarded you this briefing, consider subscribing here.

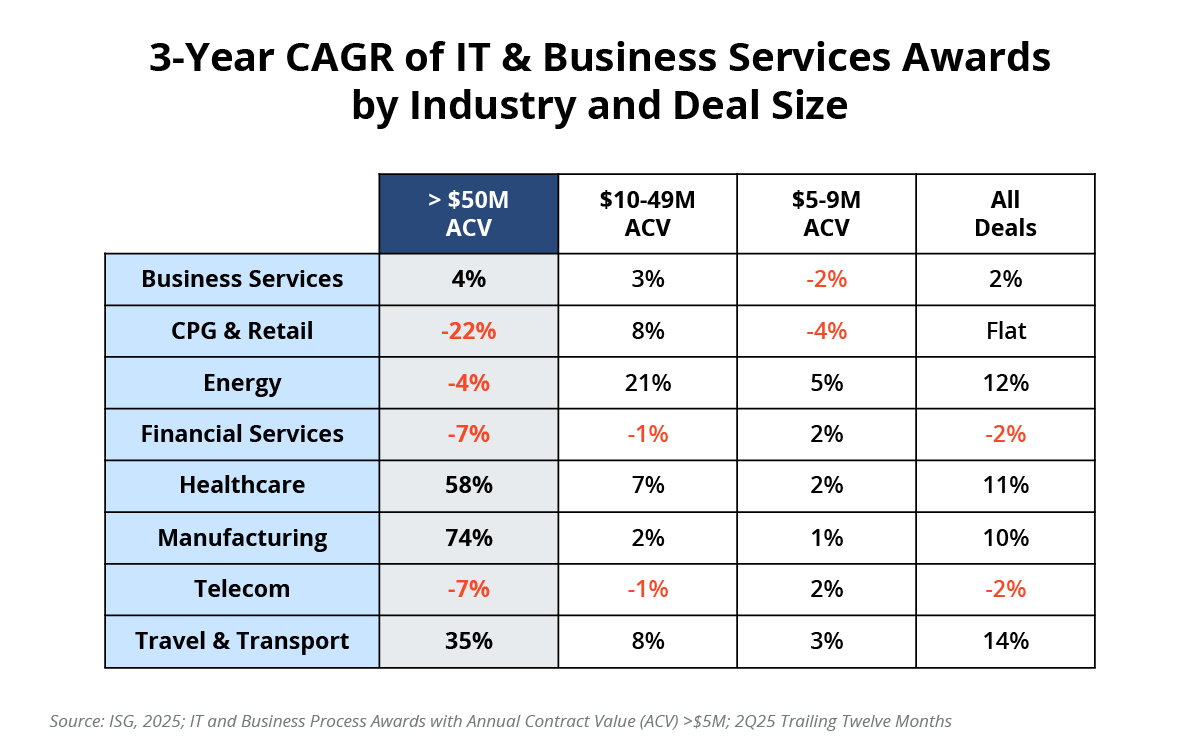

Contract Value Growth

Data Watch

Background

As we discussed on the Q2 ISG Index call, large-deal activity remained robust in the first half of 2025. However, in this week’s Insider, we’re stepping back a bit to take a look at the health and growth of large-deal activity over a longer period – three years to be exact.

As you can see in this week’s Data Watch, the growth rate of deals with an annual contract value of $50 million or more (how we’re defining large deals here) has been quite uneven, with only half of industries seeing ACV growth.

The Details

- Manufacturing has seen the strongest growth in large-deal contract value over the past three years. This may sound counterintuitive given the pressure the sector is now under due to uncertainty with U.S. trade policy, but it’s important to remember that we’re talking about a three-year period, and 2023 and 2024 both saw over $1 billion of mega deal ACV. Today, we see manufacturing firms remain focused on improving productivity, reducing costs and building flexibility and reliability into their supply chains.

- Healthcare and Life Sciences have also seen strong three-year growth in large-deal ACV. As you can see in this week’s Data Watch, contract value for $50M+ awards is up nearly 60%. This type of large-deal activity, in Healthcare specifically, was uncommon three years ago, but lately this sector has been embracing managed services at a record pace.

- Large-deal contract value in Financial Services has declined, while small and medium-sized deals have stayed relatively flat. BFSI bookings were back in positive territory in 1H25 after a tough 2024, but large-deal activity continues to be sluggish in this sector, with ACV for the largest deals down 7% over a three-year period. That said, it’s important to keep in mind that this sector was under significant pressure last year, so this “flattish” result could indicate that BFSI has almost fully recovered from 2024 lows.

- CPG and Retail have seen the biggest decline in large-deal ACV over the past three years. Large-deal activity in these two sectors is down more than 20%. Still, deals in the $10-$49 million ACV range are up, with CPG being slightly more consistent than Retail over the past year. We’re seeing a strong interest in building and or scaling global capability centers by CPG and retail firms that are looking to reduce costs while scaling AI and machine learning talent.

What’s Next

As we discussed last year, large deals make up around 25% of the ACV in the market. That means mid-size and small deals make up the other three-quarters, making them the true backbone of the sector. Overall, those deals have been resilient as you can see in this week’s Data Watch. But it’s the large deals that get the attention from the market.

And over the past couple of years, it’s been industries like Manufacturing, Healthcare and Travel that have seen growth in large deals. That could be because – overall – these industries are not as mature in their use of outsourcing as others like BFSI and Telecom. It could also be due to the fact that these sectors have faced significant cost pressure over the same period and are using the IT services sector to modernize and reduce costs.

We think this will continue to be the case, at least for the next few quarters. Large-deal activity will continue to be robust, but it will likely stay focused in a few key industries that are starting to increase their use of the IT services sector.

My colleague Sunder Sarangan and I will be holding a webinar on the topic of large-deal activity on Wednesday, August 6 at 11:30 AM ET. Reach out to my colleague Aroob Fatima for more details.

About the authors

Stanton Jones

Stanton helps enterprise technology leaders, IT service providers and buy- and sell-side professionals make sense of the global IT services sector. Stanton's weekly briefing - the Index Insider - is read by thousands of industry stakeholders each week.